This article is published in the GRG Remuneration Insight.

Introduction

For all employees and particularly executives, superannuation fails to meet retirement saving needs and no other element of remuneration focuses on this need. Retirement savings is the weak element of executive remuneration and is such a critical issue for most executives that it should no longer be ignored.

Retirement Savings Needs

The amount needed to have been saved during employment to be an independent self-funded retiree is a complicated calculation with many variables depending upon individual circumstances. Nevertheless, a long standing broad guideline has been that the retirement savings pool accumulated at retirement needs to be between 5 and 10 times final annual earnings, for an individual to be able to support themselves in retirement. This long standing view is now probably on the low side due to people living longer, higher cost lifestyle expectations in retirement and investment returns being lower than in previous decades. The retirement savings pool is in addition to home ownership which may add to the retirement savings pool if retirees move from high value to lower value accommodation.

Expenditure during retirement should be sourced firstly from the earnings from investment of the retirement savings pool and secondly from depletion of the retirement savings pool itself. Given uncertainties as to the period for which the retirement savings pool will need to fund retirement expenditure it would generally be prudent to minimise drawings from the pool and to rely mainly on the earnings from the pool. Of course, the retirement savings pool will in many cases need to support a surviving spouse as well as the executive in retirement.

Ignoring both the impact of inflation on living costs the income that would be generated from a 5 times Base Package retirement saving pool would be between 25% (5 times x 5%) and 50% (10 times x 5%) of final average earnings, if the earnings were at a rate of 5% per annum or between 50% (5 times x 10%) and 100% (10 times x 10%) if the earnings rate were 10%.

For purposes of this GRG Remuneration Insight we are going to assume that the optimal retirement savings pool is 10 times final Base Package/Fixed Annual Remuneration. It should be noted that the Base Package will be a proportion of the executive’s total remuneration package and therefore the 10 times multiple is a lesser multiple of the executive’s total remuneration package.

The Retirement Saving Gap

To accumulate the desired retirement savings pool will require significant savings per annum during the working life of an executive. Given that the income received by an executive increases significantly when the person makes the transition from a general employee to an executive it is likely that any superannuation accumulated as a general employee will be a minor component of the retirement savings pool and for purpose of this GRG Remuneration Insight it will be ignored. Therefore, the savings during the period of service as an executive will be critical to whether the desired retirement savings pool is achieved.

If an individual serves say 30 years in executive roles then the desired retirement savings pool will need to be accumulated over that period. A period of 30 years has been assumed to be a reasonable average period of service in executive roles and is based on the assumption that the person achieves an executive role by the time they are 35 years of age and remains is such roles until they are 65 years of age. Of course, there will be many individual variations in relations to these assumptions but the 30 years is seen by GRG as a reasonable period for illustrative purposes.

To achieve a retirement saving pool of 10 times Base Package an executive will need to be saving 20% to 30% (10 times Base Package ÷ 30 years = 33.33% p.a.) of the Base Package each year. Assuming that the real value of retirement savings is growing (i.e. after tax savings grow at a rate faster that the rate of growth in Base Packages) the required rate of net of tax savings will need to be less than the 33% indicated in the simple calculation in the foregoing. Present rates of superannuation contributions fall well below 30%, leaving an enormous shortfall/gap in retirement savings. If this gap is to be filled as part of remuneration packages then the fact that tax will be payable on remuneration needs to be taken into account. For example, if 10% of a Base Package is allocated to retirement savings then it will result in 5.3% (10% – 47% tax) of the Base Package being saved if the full top marginal tax rate applies.

For illustrative purposes the tax impact and the growth in the retirement savings pool from investment of earnings will be ignored on the assumption that they will act to counterbalance each other.

The attachment to this GRG Remuneration Insight contain illustrative calculations that indicate that retirement savings in addition to maximum superannuation contributions need to be around 20% (10% to 25% range) of Base Packages. These calculations also ignore the fact that higher income earners (income above $300,000 per annum) pay double (30%) the tax on superannuation contributions that take the total of salary and super above $300,000 that is paid by lower income earners (15%). The $300,000 threshold for higher tax on super contributions may be lowered as part of the 2016 Federal Budget. It should also be noted that a more detailed analysis of retirement savings through remuneration is likely to show a need for higher levels of retirement savings when taxation is fully taken into account.

Remuneration Profile Remedy

Employers can help address the retirement savings gap by mandating that:

- SGC superannuation contributions will form part of Base Packages – this is currently standard practice,

- Concessional superannuation contributions in addition to SGC contributions up to the concessional contributions cap must be taken as part of Base Packages (this aspect could be optional as the amount available for additional superannuation contributions is being eroded due to the indexation of the SGC contributions maximum and the non-indexation of the concessional contributions cap), and

- An additional component of total remuneration packages will be provided to supplement retirement savings.

The additional retirement saving component of remuneration will need to be funded by a reduction in incentive award opportunities so as not to involve employers in additional cost. Further, to counterbalance the loss of motivational impact that would otherwise arise from the reduction in incentive award opportunities it is GRG’s view that the supplementary retirement savings should be via acquisitions of equity in the employer company. Fortunately, the employee share scheme (ESS) taxing provisions support the use of equity as supplementary retirement savings.

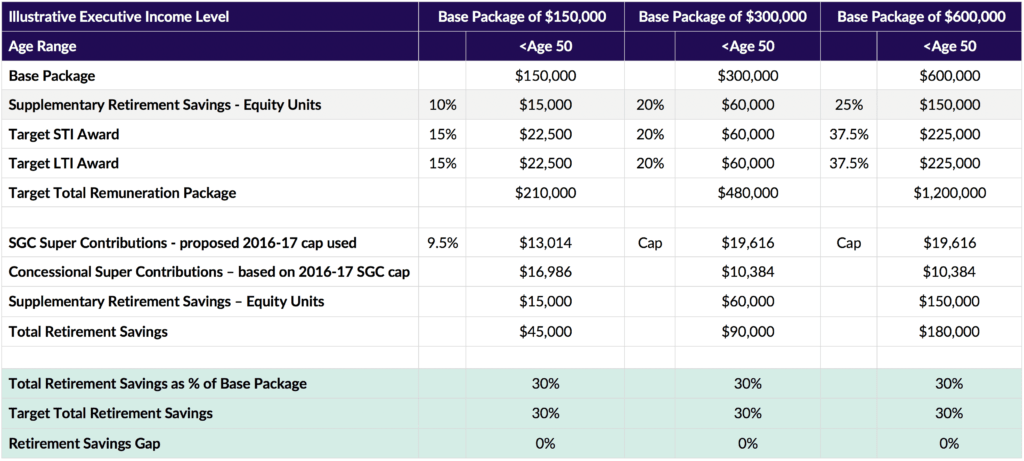

When considering the following table it should be noted that each of the three Base Package levels are intended to be representative of executives in different sized companies rather than different levels of executives in the same company. This aspect is important as the same supplementary retirement savings percentage should be applied to all executives in the leadership team of a company with the exception of the Chief Executive Officer who may attract a higher percentage.

The following table shows that:

- The retirement savings gap can be covered within existing company remuneration cost structures,

- The impact on target incentive opportunities is relatively small,

- Company cash flow will be improved as supplementary retirement saving should reduce cash costs, if new issues of shares are used.

On a “salary sacrifice” basis, part of Base Packages and/or cash STI awards could be redirected into supplementary retirement savings. This could be particularly helpful for executives who feel that their retirement saving will otherwise be inadequate for their needs.

Stakeholder Perceptions and Approvals

As this is a relatively new concept for executive remuneration packages it is not possible to guarantee that proxy advisors and other stakeholders will react to the introduction of a retirement savings element as an addition to Base Packages. Given that it will not increase the cost of remunerating executives, increases their equity interest in their employer companies and fulfils a vital social need it would be surprising if they objected in any way to the introduction of a retirement savings component to executive remuneration.

Shareholder approval of the plan would be required as would grants of equity units to directors when those equity units may involve a new issue of shares.

Conclusion

There is a strong need in Australia for companies to take a pro-active approach to ensure that executives are engaged in programs that will enable them to accumulate retirement savings pools that are adequate for their retirement years. Executives should be independent self-funded retirees who do not need to rely on social security benefits provided by government.

There is inadequate scope to accumulate adequate retirement savings pools through superannuation as it is severely limited by legislation. However, there are alternatives that can and should be considered by employers using concessionally taxed equity accumulation programs.

Details of possible approach will be outlined in subsequent GRG Remuneration Insights.

Appendix – Quantifying the Retirement Savings Gap

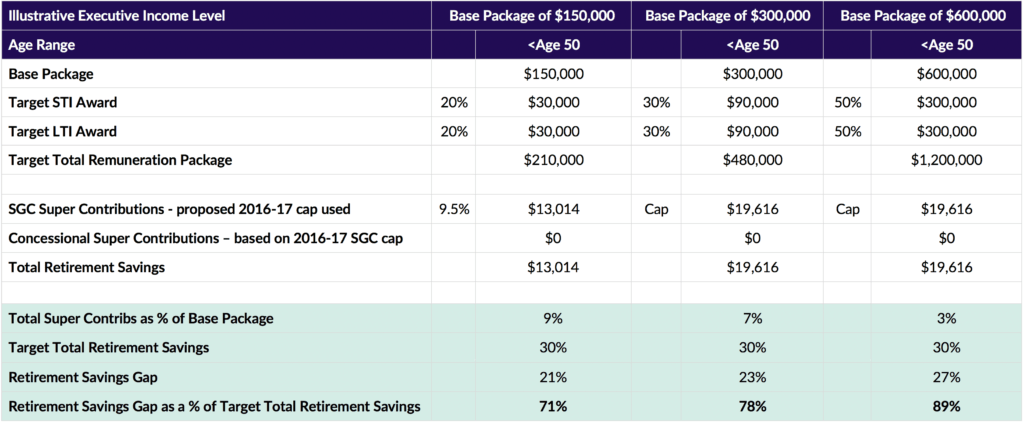

The following illustrations firstly examine the positions of executives who do not have superannuation contributions other than those required under the superannuation guarantee contributions (SGC) legislation i.e. currently 9.5% of salaries up to $206,480 per annum for the 2016-17 financial year. Three Base Package amounts are considered being $150,000, $300,000 and $600,000 and it is assumed that the executive is less than 50 years of age. Base Package includes superannuation contributions, therefore the salary component on which SGC superannuation contributions are calculated will be approximately 91.3% of the Base Package if no other benefits are provided as part of the Base Package. The target short term incentive (STI) and long term incentive (LTI) percentages are indicative of market practice and are aimed at determining indicative target total remuneration packages.

For all levels of executive income superannuation is totally inadequate in items of providing a retirement savings pool. The further that these executives are through their main retirement saving periods (30 years in the illustrations) the more challenging it will be to achieve the desired retirement savings pool. Their positions will be much worse than those indicate above which in effect relate to executives at the beginning of their 30 year main retirement saving period i.e. executives around 30 to 35 years of age. Older executives will be in much worse positions unless they have adopted supplementary savings programs.

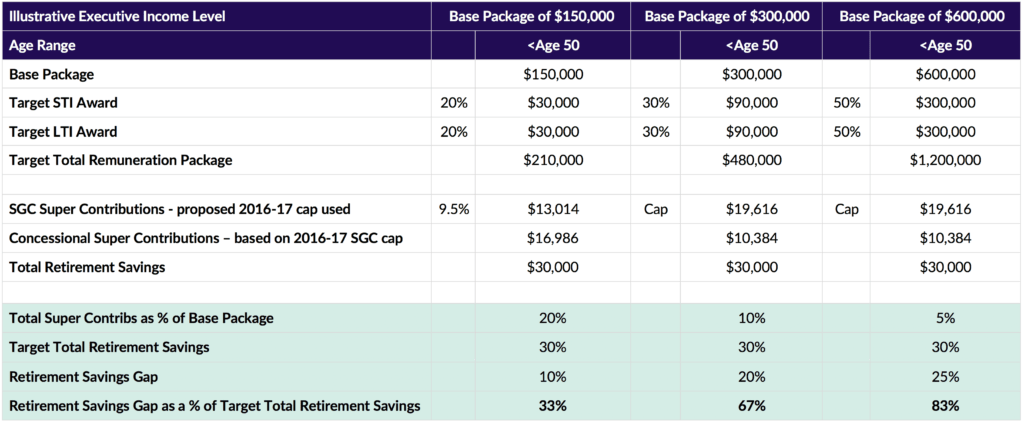

The next illustrations assume that executives are maximising their superannuation contributions by sacrificing salary into super up to the concessional age based limit.

The above illustration shows that executives who have been and will continue to maximise their superannuation contributions up to the relevant concessional limit will make better progress toward reaching the target retirement saving pool but will still fall well short of the required amounts.

These illustrations confirm the need for supplementary retirement savings plans for executives.

This article is prepared by Godfrey Remuneration Group Pty Limited. Click here to view the article or visit https://www.grg.consulting/. Contact GRG on +(02) 8923 5700 for more information.

Authors:

Denis Godfrey, Managing Director

James Bourchier, Director

Contributors:

Nida Khoury, Director

Peter Godfrey, Senior Consultant